Everyday money

Home loans

Buying your first home is an exciting journey. We want it to feel more like an epic adventure than a side hustle. Our lending specialists can help get you started with the right home loan.

Check below for a step-by-step guide to buying a property which may help you crack what all the jargon means. Use our calculator to see what you could afford and get the lowdown on the property market from our helpful tips and guides. You can even apply easily online.

Use our calculator to figure out how much you could afford

Consider extra costs and potential grants you could be eligible for

Get any final inspections, put in your offer, and pay the deposit

Once you’ve found your property, get the final “ok” from your bank

Lock in your home loan by signing the final paper work

Purchase of property is complete – its yours now, time to move in!

Let’s crunch the numbers. Just input your income and expenses, and our borrowing calculator will estimate how much you could borrow and what the repayments would be.

Important:The estimated amount you could potentially borrow is a guide only. This calculator doesn’t take into account your individual circumstances. The interest rate applied is the current interest rate for a ubank home loan with principal and interest payments and varies depending on the product you have selected. This calculator assumes principal and interest repayments. Rates and repayments are indicative only and subject to change. If you proceed with a home loan application we’ll ask you to provide further details of your income and expenses. If you want to know more, check out ‘Additional calculator information’ below. Refer to ‘Lets pass the mic to our lawyer’ for important information on our Comparison rates.

Find out about government help you might be able to get based on your state

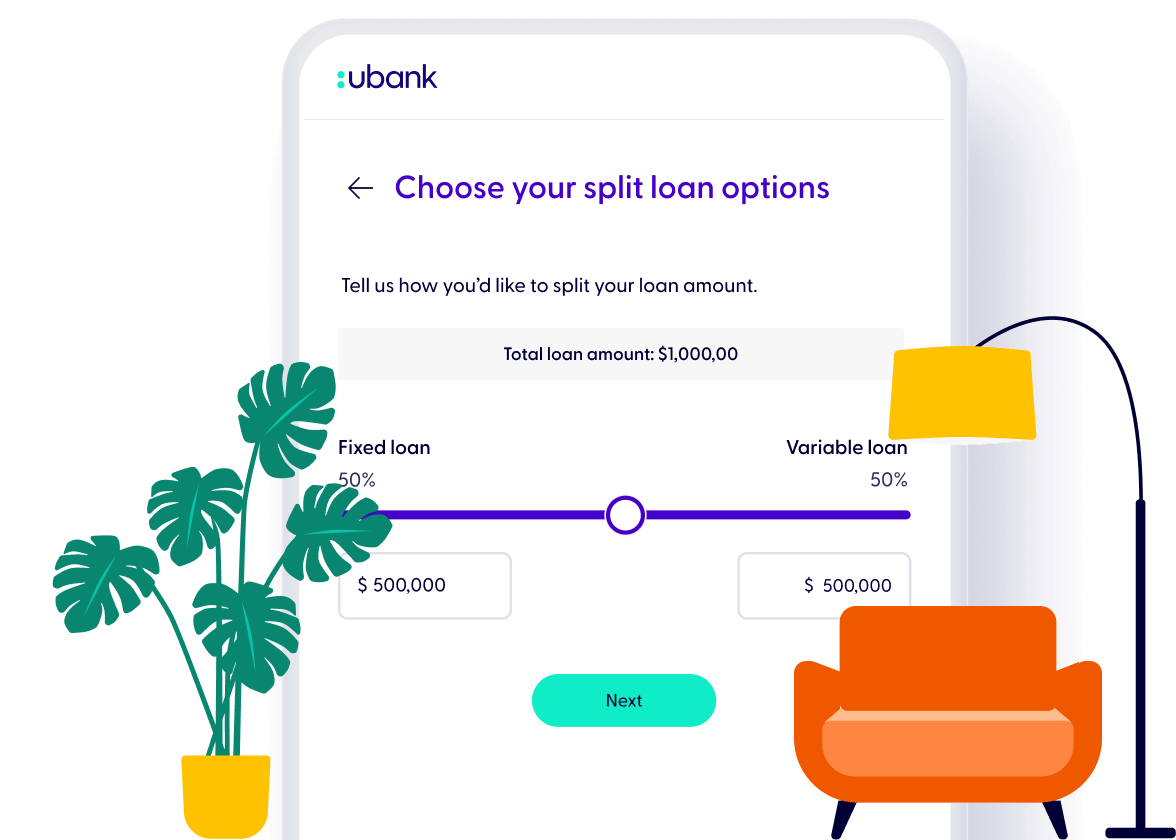

Get a mix of options with a great value award-winning home loan

With an offset account(s) and unlimited repayments (on a Flex Variable rate loan)

Get help from a friendly member of our Australian-based team, 7 days a week

Apply online or talk to our specialists for a quick decision and easy application

Our customers reap the benefits of our award-winning home loans.

Read our eligibility criteria and see if you’re eligible for a ubank loan

Easy online application or talk with a lending specialist

If your application hits the mark, you’ll get an approval fast

Hit the open houses with full confidence in your finances

Talk it over with one of our lending specialists.

Monday to Friday 9am-8pm, Sat and Sun 9am-6pm (Syd time)

.svg)

The maximum loan amount is an estimate and is indicative only, based on the income and expenses you have entered.

It doesn’t take into account loan eligibility criteria or your complete financial position. Borrowing power calculation does not constitute a loan offer.

We have also made a number of assumptions when estimating your borrowing power and those assumptions affect how reliable this estimate is. These assumptions include:

Your income

Your expenses

Interest rates

Repayments

Repayments are indicative only. When calculating repayments we have had to make a number of assumptions which may affect the accuracy of the amounts shown. They include:

Fees and charges

Read our Home Loan Terms.

Credit criteria, fees and charges apply. Applicants must live in Australia and meet eligibility requirements.

Home loan information and interest rates are subject to change.

1Comparison rates are calculated on a loan amount of $150,000 for a term of 25 years. These rates are for secured lending only.

WARNING: The comparison rates are true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

For a personalised comparison rate that applies to your proposed loan, see the Key facts sheet.

Comparison rates for variable interest only loans are based on an initial 5 year interest only period. Comparison rates for fixed interest only loans are based on an initial interest only period equal in length to the fixed period. Interest rates are applicable at the time of loan approval and are based on the loan to value ratio (LVR). The LVR is the amount of the loan compared to the property value expressed as a percentage.

Do it all from home with our simple digital loan application.